By Robert Thomas

This blog provides an update on the handling of tax credit checks by Concentrix. It also presents and considers newly released data concerning the outcome of mandatory reconsiderations decided by Concentrix.

Earlier in 2016, concerns were raised about tax credit compliance checks undertaken by a private company, Concentrix, on behalf of HM Revenue and Customs (HMRC). For a detailed background, see this blog here. People in receipts of tax credits had been contacted by Concentrix and many then had their tax credit payments cancelled, resulting in particular hardship. This led to many complaints to MPs and public concern about the nature of these checks and the approach of Concentrix. The problem was that Concentrix had been stopping tax credit payments, often for no good reason.

Background

According to a recent report by the Commons Work and Pensions Committee, vulnerable people had lost benefits to which they were entitled, through no fault of their own. Some people had been put through traumatic experiences as a consequence of avoidable failures. There were both customer service failures and decision-making failures. The Committee concluded that tax credit claimants seeking to ensure continued eligibility for tax credits were faced with a decision-making system stacked against them:

- the merest hint of financial association between a claimant and another adult in the household could be enough to trigger a Concentrix compliance check;

- similarly, claimants were targeted on the basis that they merely shared some characteristics with unrelated fraud or error cases;

- such claimants were sent letters informing them their tax credits would be stopped unless they could prove within 30 days that they were entitled to them;

- they were treated as guilty until proven innocent;

- claimants seeking to prove their eligibility were not informed of the full basis of the suspicions against them, such as the identity of a possible undeclared partner; and

- such claimants were tasked with proving the negative that they were not in a relationship with someone with some form of connection to them.

To reduce the amount of error and fraud in the tax credits system, HMRC had contracted with a private-sector supplier, Concentrix, to undertake checks to prevent overpayments and inaccurate claims and fraud. However, the principal result seems to have been to increase the degree of error through poor decision-making. On 11 November 2016, HMRC announced that it had ended its contract with Concentrix.

There is a wider issue here of the contracting out of public functions to private companies and in particular contracting out of welfare functions. As the Commons Work and Pensions Committee concluded:

‘We have grave concerns about the delegation of benefit decision making to private companies. This is especially true when payment structures incentivise the removal of benefits. We welcome HMRC’s commitment not to use private contractors to make benefit decisions in future.’

The Committee also stated that ‘this was the first time such a high degree of decision making authority with regard to benefit claims was delegated to a private company. It was not a successful experiment.’

There is also a specific administrative justice issue. In addition to undertaking compliance checks, Concentrix was undertaking mandatory reconsiderations when a claimant challenged the initial decision. The contract between HMRC and Concentrix was on a payment-by-results basis. This gave rise to the suspicion that Concentrix would be motivated by a desire for profits when undertaking mandatory reconsiderations. As the Social Security Advisory Committee (SSAC) in its report on mandatory reconsideration (July 2016 at page 39) put it:

‘When claimants disagree with a decision and request an MR, it could be argued there is an incentive for Concentrix staff not to overturn decisions given it would impact negatively on their revenue. Put another way, the profit motive could reduce the ability of the contracted out organisation and its staff to be impartial when reconsidering decisions.’

This could be called the ‘profit motive’ theory of privatised administrative justice: private contractors undertaking administrative justice functions on behalf of government are likely to exercise those functions to further their own interests – in particular profit maximisation. Government departments are motivated by a public-service ethos. By contrast, private providers are under no such obligation and are far more likely to be motivated by a desire to increase their profits.

Newly released data

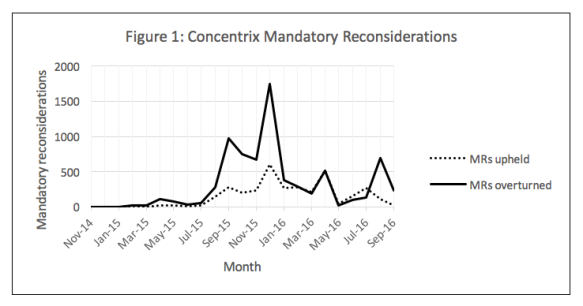

When it published its report, the SSAC did not have any data concerning mandatory reconsiderations undertaken by Concentrix. However, following a recent FOI request these data have now been released by HMRC and are provided here.

Since the commencement of its contract in November 2014, Concentrix started investigations on 948,003 claims. Out of those claims, Concentrix decided some 10,823 mandatory reconsiderations between November 2014 and 13 September 2016. This amounts to 1.14% of all of its investigations. Of those 10,823 mandatory reconsiderations, 32% of initial decisions were upheld and 68% of initial decisions were overturned.

Figure 1 shows the number of mandatory reconsiderations upheld and overturned by Concentrix by month. ‘MRs upheld’ refers to mandatory reconsiderations in which the initial decision was upheld and ‘MRs overturned’ refers to those in which the initial decision was overturned.

What the data tell us

The following points can be made:

First, contrary to expectations, the data clearly do not support the ‘profit motive’ theory. It is clear that there might well have been an incentive for Concentrix not to overturn decisions in order to increase its profit. However, if this incentive had exerted any influence, then we would have expected to see more initial decisions upheld than overturned. The data do not bear this out at all. On the contrary, a far greater proportion of initial decisions have been overturned than upheld. Accordingly, this tends to undermine rather than support the ‘profit motive’ theory. According to HMRC, the number of overturned mandatory reconsiderations is broadly in line with the number overturned in HMRC.

Nonetheless, this should in no way be seen as a green light for the future. For instance, the proportion of initial decisions that went to mandatory reconsideration was a very small and self-selecting sample of decisions. One possibility here is that mandatory reconsideration decisions were undertaken by a better qualified team within Concentrix and/or one which was not placed under pressure.

Second, the success rate for claimants raises familiar concerns about the quality of initial decisions. Such concerns were voiced by the Commons Work and Pensions Committee. According to the Committee:

‘The flaws in decision making are evidenced by the fact that more than 90 per cent of initial appeals (sic), known as Mandatory Reconsiderations, against Concentrix decisions in HRR16 have been upheld. These are extraordinary figures for any appeals process, let alone one that left people in hardship as their benefits were stopped in the meantime. Yet those rates were accepted by both Concentrix and HMRC as a routine feature of the system.’

(HRR16 refers to High Risk Renewal, a cycle in which Concentrix considered a subset of claims.)

There is a long-standing issue here as to whether administrative justice processes give us an accurate insight into the quality of initial decision-making. According to HMRC, the majority of cases overturned by Concentrix occurred as a result of customers providing new required information. If so, then the mandatory reconsideration process becomes an assessment of new evidence not before the initial decision-maker. Consequently, it could be argued that the headline success rate is not a clear indication of the quality of initial decision-making. Nevertheless, it is clear that there were significant problems in the decision-making process. Furthermore, initial decision-making should ideally collect any relevant evidence upon which to make a good, decent decision. Otherwise, resources are wasted through poor decisions.

A third point is that only a small proportion of claimants sought a mandatory reconsideration. What of those who did not? How many other people are in receipt of a decision that could be successfully challenged? It would be understandable and unsurprising if many claimants, having experienced the initial compliance checks undertaken by Concentrix, then lacked faith in a mandatory reconsideration process itself undertaken by Concentrix. But many people do not challenge negative decisions in any event.

This is a major issue of administrative justice and was discussed in a recent report on administrative justice. The administrative justice system rests on the principle that people will challenge poor decisions. But many people do not challenge and they stand the risk of losing out because of it. At least part of the solution is for initial decision-making bodies themselves to introduce effective quality assurance systems to review and check the quality of their decisions, irrespective of whether or not they are challenged by claimants. This finds support from the Commons Work and Pensions Committee, which noted that ‘Many claimants may have not, for a range of reasons, submitted an appeal (sic). We recommend that all Concentrix decisions in HRR16 to stop tax credits that have not been appealed are reviewed by HMRC.’

Effective use of quality assurance could be a major way of advancing administrative justice. However, in a good illustration of how far away we currently are from this, consider HMRC’s monitoring of Concentrix. According to the Commons Work and Pensions Committee, HMRC has monitored Concentrix decision-making but only on narrow technical grounds, and on those terms HMRC was satisfied that its contractor was doing a good job. As the Committee noted: ‘Rather than being concerned that Concentrix were wrongly identifying fraud and error, HMRC expected their contractor to find far more instances than they did.’

A final point is that the whole episode has highlighted considerable concerns about privatised administrative justice. The Commons Work and Pensions Committee has recommended that the Government commission an independent, root-and-branch review of tax credit compliance processes. This should incorporate decision-making and appeals, appropriate evidential burdens and timescales, and the effects on claimants. According to the Committee, ‘This was a sorry episode for the welfare state. It is imperative that it is not allowed to happen again.’

About the author:

Robert Thomas is Professor of Public Law, University of Manchester.

Discussion

Trackbacks/Pingbacks

Pingback: Joe Tomlinson: The Gap between Promise and Performance - Strong, Weak, Modest and Sham Systems of Administrative Justice | Administrative Law in the Common Law World - July 3, 2017